Hi there,

First and foremost, we’re happy to report that we’re both healthy and well, and that the same goes for our family. We’re (safely) drinking a beer and looking out at the Pacific.

We hope you all are well too, and hope this letter will bring you a chortle and even perhaps a nugget of insight into global markets. Clearly, we’ve fallen off with this newsletter, which betrays the core principle of any such endeavor, consistency. We can’t promise we’ll get that back.

But… we do love dropping in from time to time, if you’ll allow us.

Here’s our vantage point on markets and what 2021 may have in store.

Fearful Symmetry

In many if not most ways, we expect 2021 to look a lot like 2020.

The pandemic will continue to be a scourge on our lives, both individual and collective, impacting small businesses especially in staggering ways.

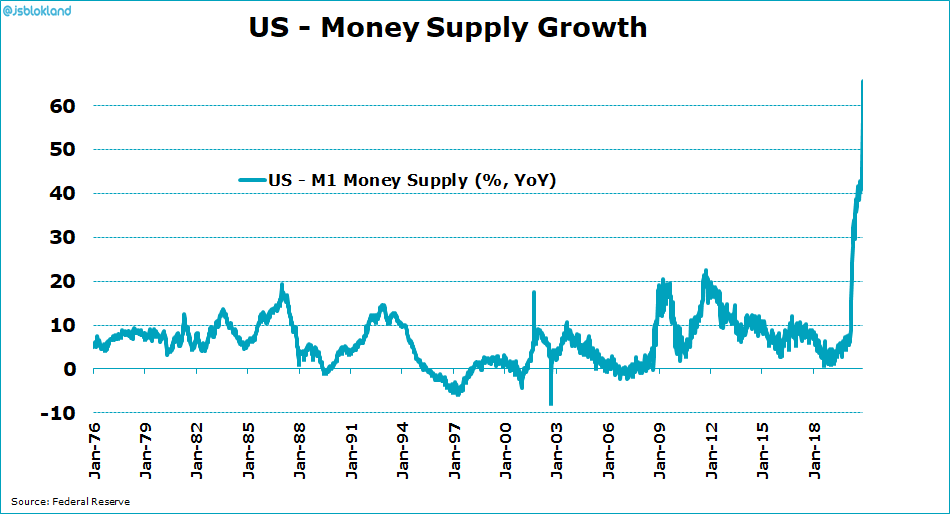

In an effort to bolster the financial system and anesthetize growing US deficits, the Federal Reserve will continue to print.

This money functions more to back-stop banks; it doesn’t flow directly into the economy. I.e. absent bank-lending, a lot of this ‘new money’ just stays on bank balance sheets.

Still, while monetary and financial asset inflation haven't yet been paralleled by inflation in consumer goods and services (and may not for some time), their sheer scale looks like a tinderbox waiting for the right (or we should really say wrong) set of catalysts.

Knowing this, investors have and will continue to deploy cash before rather than after inflation comes, hoping not to get caught holding depreciating cash assets. Primarily, this money has flowed to super high-growth companies (which we wrote about in one of our notes from June).

Stretching for the highest possible growth makes sense when you consider the pace of monetary inflation that investors are trying to out-run:

Still, despite all this printing, the idea that the dollar is somehow dead, much like the idea that New York City is dead, is also overblown.

As the entire world grapples with the pandemic, the European Central Bank, the Bank of Japan, and the like are all equally hard at work buttressing their respective financial ecosystems — printing lots of currency of their own.

If everyone’s doing it, aren’t we all staying at sea level?

That’s where Bitcoin has again surged, nestling into a niche as a potential reserve currency alternative, and cresting well above its previous highs from 2017.

Another fact we barely need mention is that interest rates have been and will continue to be six feet under for years to come. This does wonders for almost all financial assets, while doing little to reduce (or actively worsening) inequality, whether between rich and poor individuals or big and small businesses.

While they won’t change rates, an equal part of what the Federal Reserve and other CB’s focus on is their ‘communication policy,’ namely setting future expectations.

That’s where we see the possibility of some shifts in 2021. Recognizing that they’ve already lost control of the narrative around inflation, with the complete meme-fication of their money printing, the Fed may well take a more hawkish tune about future interest rate increases or other policy changes.

That will generate lots of Bloomberg headlines and maybe, short-term consternation in markets. Which you should ignore as noise. Whether you’re in it for the long hall, or not that deep in it to begin with, none of that really matters :)

Now, let’s chop it up a bit more.

For the first part of 2021, we expect stocks to hum along (as they did for the first quarter of 2021. We see markets going as high as SPX 4,200 or even 4,500 in the near-term, with the speculative boom across asset classes and bleeding-edge companies reaching a fever pitch (and in many ways following bitcoin). Momentum alone can be powerful, as we’ve seen throughout this year and frankly, this decade. So what’s not to love?

At some point, whether it’s a new virus variant, or something equally unforeseen as the ultimate impact of COVID-19 was in 2020, the next shock will come around to occasion a fundamental re-rating of financial asset valuations. We communicated as much at the end 2019, and expect this will clear out a lot of the ‘dreck’ that’s out there in asset valuations (as of Sunday, 1/3, $SNOW was a $85B company on $500M in sales).

Valuations will come down, whether in 2021 or 2031.

But re-ratings of financial asset valuations aren’t always to the downside, either.

One lasting impact of coronavirus on financial asset prices will likely be a meaningful, clear shift in investors’ calculus of how to value consolidated, leading companies like Apple and Amazon, as well as innovative companies at the fore-front of technology. In 2020, in both cases, a resounding chorus of investors sang, ‘We’ll pay up’.

It took a pandemic for investors to fully appreciate that Apple is a high-margin juggernaut and should be priced accordingly. Despite already starting as the largest company in the world, it’s value has basically doubled this year, expanding its P/E multiple from 20x to 40x.

Similarly, it took a pandemic to illustrate just how entrenched Amazon is across the U.S. It’s value has also effectively doubled since March.

With respect to the second basket of companies, i.e. those at the bleeding edge of various sectors, the important thing to remember is that in the grand scheme of things, we're in the very early days with respect to things like the internet, or healthcare tech innovation. It just feels late from our single-lifespan perspective. Companies we've covered in these pages, like $NVTA, as well as countless others, are doing amazing things, and are getting bid up handsomely as a result. Their valuations will fluctuate, but as the pace of global innovation quickens, investors aren’t waiting for companies to prove their theses out 100%. No one wants to miss the next Apple or Amazon (as above). So especially with relentless elimination of traditional gatekeepers to markets, increased public participation drives fundamentally different investment behavior and valuation dynamics.

Another major focus for us has been how the pandemic has accelerated Bitcoin’s global role and position. Up ~400% in 2020, Bitcoin was one of the best performing assets of the year (although it’s still no Tesla, which was up nearly 700%). 2020 saw an undeniable correlation (whether functional or purely psychological) between fiat money printing and Bitcoin adoption, as investors, institutions and speculators alike flocked to the asset partially due to its fixed 21M coin supply, a stark contrast from the previously shown money supply chart.

The culture is buying in as well. As we mentioned in August, the Dave Portnoy x Winklevoss twins interview may have been a watershed moment in the public zeitgeist.

But there is a signal beyond all this noise that is proving Bitcoin’s worth as a store of value and increasingly as a medium of exchange. Payments company PayPal is enabling Bitcoin transactions for its online merchants and 346M active accounts, providing a major distribution channel for consumers and merchants alike to transact with bitcoin. The company is joining the likes of Square, which already attributes nearly a quarter of its revenue to its bitcoin service and recently decided to hold $50M of bitcoin on its balance sheet. We expect to see more of this institutional adoption in 2021, and we expect to see continued technological progress like the growth of the Lightning Network.

Whether Bitcoin truly goes to the moon next year is beyond our paygrade, but its comparison as the ‘digital gold’ has become increasingly interesting and in our opinion, holds merit. Gold has a market capitalization of nearly $10T, to Bitcoin’s $350B. Even just a shift to 90/10 would look like 3x upside for Bitcoin. Plus, we’re talking largely about psychological shifts here — gold’s value, much as bitcoin’s detractors say, is largely a function of perception (though it does have a significant lindy effect tailwind). We remain bullish on it long term — where the price will settle at 2021 year end is anybody’s guess, but we do not expect to fully repeat the 2018 doldrums that followed the 2017 runup. That said, it’s price has gone up 30% since we started writing this, so we dare say there’ll be hiccups to accumulate more coin.

Give us the goods.

So, what investing are we doing in 2021?

Good question. With portfolios that have become quite overweight tech, we’re looking at four baskets, based on three dimensions, namely diversification, adjacency to emerging / explosive trends (e.g. EVs), and inflation-resistant if not antifragile assets.

Big Diversified, Compounders at passable prices:

The pandemic will continue to drive consolidation in favor of large co’s (unfortunately). And there’s still great co’s out there that trade 20-30x PE

Getting closer to real assets again, whether in metals (precious and industrial alike), food and agriculture, and energy. This basket three distinct advantages:

Metals are of course an inflation + infrastructure play, but the right miners can enjoy nice tailwinds from major global shifts, such as the boom of emerging markets (copper, iron ore), or EVs (lithium, other rare earths).

AG + Food plays cover for inflation, benefit from pandemic consolidation and should stand the test of time as the world population balloons anyways.

When we say energy, for our purposes we’re talking alternatives like wind, solar, (and even uranium, as part of what we expect to be a shifting energy consensus). These benefit from inflation and demographic changes.

If you have no qualms investing in good ol’ fashioned crude + crude oil companies, well, we reckon they’ll fair well in the short-term too.

Will 2021 herald the end of the commodity bust cycle? We’ve been waiting.

Small / Micro-Cap Moonshots:

Niche medical research

Frontier markets

Bleeding edge tech when we can find great companies before they blow up, e.g. $FSLY circa this time last year)

Alternatives: We’ve discussed BTC, but in no particular order, we also love RE, VC opps, and increasingly, our own projects ;).

If you want to chat ideas here, give us a shout. And if you send us a smidge of Bitcoin, we’ll provide you with our asset shopping list for the week of Jan 4th.

If you take nothing else from this, then let it be our best wishes that you all stay healthy and well. Your health is worth a billion dollars. Invest in it. Onwards.

Be in touch. We appreciate you,

Nick + Mark