'21 Check-In

Our 2021 theses have been pretty dialed. So what's next?

Hi there,

First note that we’ve rebranded as “the gravy train.” I.e. a riff on what markets have been like for the majority of our investing life. And how ridiculous and silly that can be (contrary to anyone’s strong form efficient market hypothesis). It’ll be all the more cheeky if we ever get years (as opposed to days and weeks) of poor performance in equities. Hope we aren’t setting the top here.

For today’s note, we would like to (i) calibrate on where we stand with respect to our original vision for 2021 a few months into the year (ii) propose updates to said vision. No, we’re not going to dive deep on $GME. Or NFTs. You’ll have to call us for that or hunt us down in Clubhouse rooms.

That said, there’s still some solid Bitcoin discussion in here. Since that’s all anyone cares about these days ;)

All aboard.

2021 Roadmap + Scorecard: How are we doing?

Coming into the year, we outlined our key thoughts in this brief.

These are encapsulated in the following list, which we will now re-visit and score:

Room to run in equities; SPX target: 4,200-4,500 (Score: B; tbd)

Narrative surrounding a more hawkish Fed (Score: A)

Long Bitcoin (Score: A)

Long Commodities (Score: A)

Micro-Cap / Moonshot companies (Score: A)

Large Cap Companies (Score: C)

1. SPX → 4,200 — 4,500

We won’t waste much breath here either. As of this writing, major U.S. equity indices are a mix of slightly up / flat / down (if you’re the NASDAQ) for the year. In the rest of this brief, we enumerate rationale for why we’re still near-term bullish.

2. Fed Speak

In our brief at the beginning of the year, we wrote:

Recognizing that they’ve already lost control of the narrative around inflation, with the complete meme-fication of their money printing, the Fed may well take a more hawkish tune about future interest rate increases or other policy changes.

Surely enough, the most powerful nascent narrative in 2021 so far is about inflation, and the corresponding actions the Federal Reserve may need to take.

In January, we saw headlines such as the below planting seeds in investor’s mind that the Federal Reserve may curtail its supportive monetary policy sooner than expected:

“Fed's Kaplan hopes to begin QE weaning this year” (link)

And right now, we’re seeing consternation in equity markets for the first time in months, originally sparked by yields in U.S. Treasuries making a sharp move higher. High-flying, speculative tech especially has been hurt by the prospect that money might not be free forever.

Part of the increase in yields and investors’ concern about tighter monetary policy is tied up in another one of our visions for 2021 and beyond, namely a boom in commodity prices. This is now well underway. This surge in commodity prices has ignited higher inflation expectations (as raw material prices can eventually move through the supply chain and show up in consumer prices).

Do we think the Fed can or will actually increase rates or reduce it’s QE bond purchases in the short-term? Probably not. Especially as:

Other central banks around the world unroll even more accommodative monetary policy (see the RBA’s announcement from Monday)

Inflation in consumer prices isn’t apparent nor unassailably obvious yet

The U.S. deficit balloons to fund COVID relief

That said, we’re more closely monitoring shifts in the Fed’s tone than we were previously.

On Thursday, Jerome Powell conceded that re-opening could increase inflation “temporarily.” While that still seems like temperate messaging, it’s a far cry from the below, which he noted a few weeks ago:

“Powell says inflation is still ‘soft’ and the Fed is committed to current policy” (here)

Communication policy can’t move by leaps and bounds. Gradual concessions like Powell’s “temporarily” could build to a larger admission that the much fabled inflation is back and rates can’t be left as low as they have been. That would put more serious pressure on markets.

Why? At the end of the day, the gravy train that has been U.S. stocks and alternative assets for years now has been and is still heavily dependent on the idea that money can be borrowed for next to nothing both now and in the future.

More on that another day perhaps, as we have other scores to cover.

3. Bitcoin

Bitcoin has rocketed up more than 50% this year, more than doubling since December. While we are optimistic about Bitcoin’s future, let’s think through the near-term catalysts and how we should be thinking about the current set-up.

To do so, we’ll peruse and pursue three potentially valid lines of inquiry for BTC. You see, Bitcoin (to its credit) hasn’t precisely shown us what it is yet.

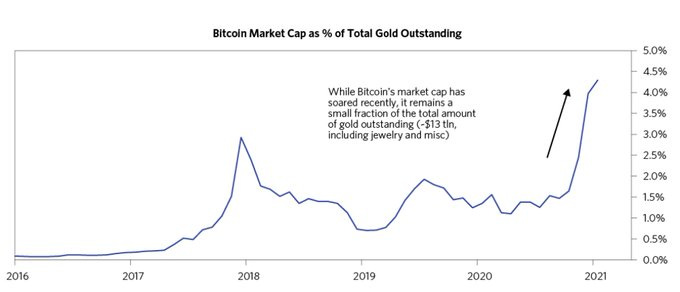

Is it a challenger to gold’s status as a global store of value?

Is it an inflation hedge?

Is it an emergent technology (a risk-asset proxy)

Let’s take a look at #1. At recent prices, Bitcoin’s total value is already approximately 5-10% of gold’s ($1T vs. ~$10T). Considering that gold has been coveted for 5,000 years and that Bitcoin has been around for less than 20, the fact that Bitcoin has already captured 10% of gold’s market share makes this theory a bit less interesting to us.

More importantly, it’s clear this isn’t a zero sum game. Gold has really struggled recently, losing ~$1.5T in market cap since the start of 2021. All of which clearly hasn’t flowed to Bitcoin (or even all cryptocurrencies combined). $1.5T = the total size of the cryptocurrency market. So there are other forces at work here, and it isn’t as simple as people exchanging their gold bullion for BTC. In sum, the idea of Bitcoin as a digital gold alone isn’t really doing it for us here.

If we think through #2 more however (BTC as inflation hedge), we see more merit.

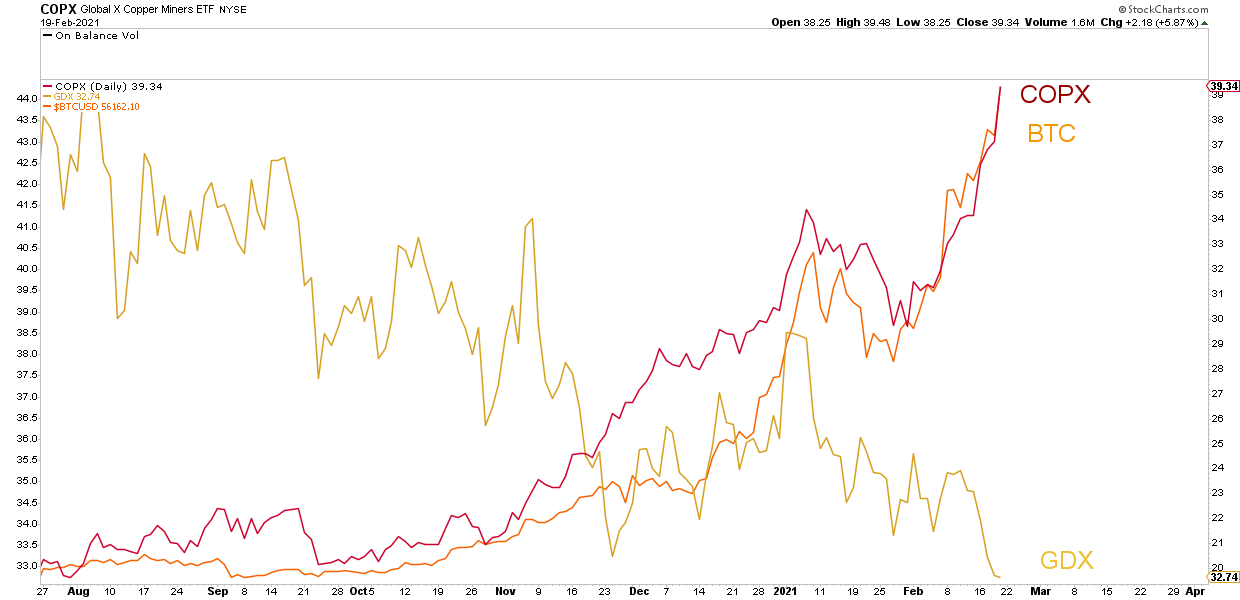

Time will tell whether or not Bitcoin will serve as an inflation hedge in an actual inflationary world. What we’re seeing at current is that people expect it to behave like one. Of late, Bitcoin has traded much more like copper than gold, as shown below.

Higher copper prices speak to a forecast of a reflationary economic environment; it’s not a pure-play inflation corollary (it’s heavily tied-to predictions for industrial activity in China and other emerging markets), but it’s one of the better gauges we have.

So in the same way commodity prices are a prediction of greater demand / shorter supply for a metal like Copper in the future, similarly Bitcoin’s price looks to us like a reasonable proxy for inflation expectations.

In other words, it’s chart looks not dissimilar to the below, albeit on a vastly different scale.

What then about our tenet #3, which centers more on BTC as a proxy for risk-assets in general (e.g. tech, speculative healthcare, etc.)? We’ll circle back on this one once we’ve spoken to the commodity portion a bit more (below).

4. A Commodity Supercycle?

In our January brief, we opined that we wanted to:

(Get) closer to real assets again, whether in metals (precious and industrial alike), food and agriculture, and energy.

We’ve written about the wind in commodities’ sales a bit already above. So, we’ll let some numbers do the work here. All % price increases are from 1/1/2021.

U.S. Gasoline: +45%

Crude Oil: +33%

Lumber: +25%

Lean Hogs: +25%

Copper: +15%

Corn: +14%

So, what’s next?

Are we headed for a deflationary environment or an inflationary one? That is the critical binary. And we don’t know the answer.

What we do know is that the narrative water in which we swim (i.e. the common knowledge coalescing all around us) has firmly shifted into a land of inflationary expectations. Every other article in main stream financial news is all about Inflation Inflation Inflation. A month ago we were still engaged in a tech-boom, roaring 20s, conversation. Maybe that will come back yet.

One outcome down the road up could be an actual break higher in consumer prices, perhaps occasioned by catalysts like commodity prices (as discussed) moving through the supply chain from manufacturers to consumers. Housing is also particularly tight in the U.S.; this could be a tinderbox as well (as explored in this worthwhile read). One potential counter-point is unemployment; as long as people are out of work and not spending, that’s a strong countercurrent vs. inflationary pressure.

But expectations alone often drive flows in markets. Once something is observed in data, it’s probably already been played forward in prices. Short-term, you’re better off positioning for an inflation positive world than a deflationary one, solely because everyone is already taking steps towards that door. Don’t get crowded out.

To refine our stance even more, let’s return to the question we posed earlier, “namely is BTC a risk corollary or inflation hedge?” We think the best answer until proven otherwise is both. We have established that BTC has a role to play as a reflection of inflation expectations. Further, the fact that Bitcoin still trades close to its all-time high as of this writing tell us that appetite for risk hasn’t left the building yet.

Lastly, it’s worth noting that there’s an incredible reservoir of cash on the sidelines (see below) prepared for one or two last surges into risk assets, especially if the Fed jumps in with some new guidance or policy.

In short — we don’t think the end-times are quite here for your stock portfolio. Our two-part thesis is:

Position for an inflationary world

Don’t get shaken out of the markets / risk-assets entirely in the coming flushes

In terms of allocations, our updates two months into the year would shift us evenly more heavily into real assets, real estate, and companies that actually make money (a rather foreign concept these days). Always happy to talk tactics more off-line.

Of course, if you own shit companies because they were pumped by some reddit army or on Clubhouse, they could continue to could get cut in half.

Scooped

Here’s what else has our eye:

Social Coins + NFTs; we’re intrigued (see here)

Universal Basic Income coin? U may need an extra cup of joe for this one

We’re also on chatting on Clubhouse a lot these days: @nickvanosdol, for one. Hit us if you need an invite <3

That’s all for us. We appreciate you and are sending you gr8 vibes. Have a lovely spring and get those beaks wet in some trades.

Best,

The blokes